Guide to the 3 Tax Funnels: Where Should Your Next Investment Go?

One of the biggest expenses in people's lives is taxes. This is not just from your salary while working but often carries over into retirement. We see a lot of individuals who retire actually be in higher tax brackets than they were while working. [see 2025 brackets here]

Taxes have a big impact on your investment returns. Where you put your money—taxable, tax-deferred, or tax-exempt accounts—determines how much you keep versus what goes to the Government over your lifetime. Understanding these three tax funnels helps you decide the best place for your next investment.

The Three Tax Funnels Explained

Your investments fall into one of three categories based on how they are taxed:

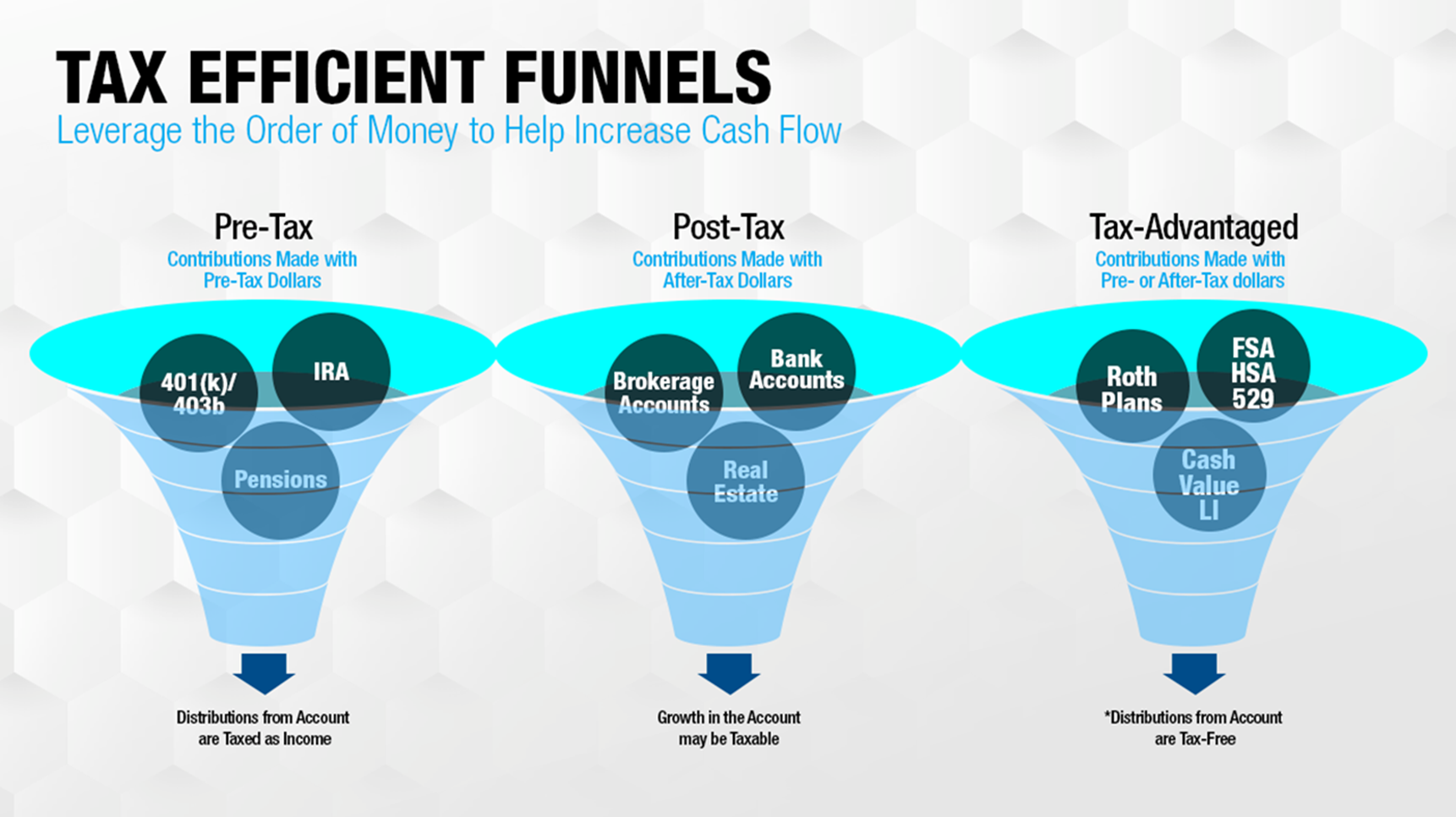

Taxable Accounts: You pay taxes on dividends, interest, and capital gains.

Accounts: Nonretirement investment accounts, Real Estate, Bank Accounts, etc.

Interest, Short-term Gains, & Ordinary dividends are taxed as ordinary income: 0% - 37%

Long-term Gains & Qualified Dividends: 0% - 20%

Related: Guide to qualified dividends & Ordinary Dividends: How they are taxed

Tax-Deferred Accounts: You defer taxes on earnings until withdrawal.

Accounts: Pretax Employer Retirement Plans (401k, 403B, Simple, etc.), Traditional IRA, SEP IRA, Pensions

Withdrawals from these accounts are taxed as ordinary income: 0% - 37%

Tax-Exempt Accounts: You pay taxes upfront, but earnings and withdrawals are tax-free.

Accounts: Roth Employer Retirement Plans, Roth IRAs, HSA, FSA, 529, Cash Value of Life Insurance

Withdrawals from these accounts are tax-free if the rules are followed: 0%

Understanding how these work and when to use each can help you minimize your tax liability every year but also over your entire lifetime.

1. Taxable Accounts: When to Use Them

What they are: These accounts include brokerage accounts and savings accounts, where you invest with after-tax money. Gains, interest, and dividends are taxable in the year they are realized.

Best for:

Short-term investments or money you might need before retirement.

Tax-efficient investments like ETFs, index funds, and municipal bonds.

Investors who have maxed out tax-advantaged accounts.

Tax Strategies:

Tax-Loss Harvesting: Offset capital gains by selling losing investments.

Holding Investments for Over a Year: Long-term capital gains rates are lower than short-term rates.

Municipal Bonds: Interest is tax-free at the federal level (and sometimes state level).

Related: Why Smart Investors Love Market Dips

2. Tax-Deferred Accounts: Pay Taxes Later

What they are: These include 401(k)s, traditional IRAs, and annuities. Contributions may be tax-deductible, and earnings grow tax-deferred, meaning you don’t pay taxes until you withdraw funds in retirement.

Best for:

High earners looking to lower taxable income now. Think of people in the 24%+ tax bracket.

Retirement savings with long-term growth potential.

Investors expecting to be in a lower tax bracket in retirement.

Tax Strategies:

Maxing Out Contributions: Reduces taxable income.

Strategic Withdrawals in Retirement: Avoid pushing yourself into a higher tax bracket.

Roth Conversions in Low-Income Years: Pay taxes at a lower rate and move funds to a tax-exempt bucket.

3. Tax-Exempt Accounts: Pay Taxes Now, Save Later

What they are: This includes Roth IRAs, Roth 401(k)s, and HSAs. Contributions are made with after-tax money, but earnings and qualified withdrawals are tax-free.

Best for:

Young investors in lower tax brackets who expect higher future income.

Investors who want tax-free withdrawals in retirement.

Those using HSAs for long-term medical expenses or 529s for future college funding.

Tax Strategies:

Roth Conversions: Move money from a traditional IRA to a Roth in low-income years.

HSA Maximization: Contribute pre-tax dollars and use funds tax-free for medical expenses.

Prioritizing Roth Contributions Early: Lock in today’s tax rates before they increase.

Where Should Your Next Investment Go?

Your choice depends on your tax bracket, income expectations, and investment goals.

The best strategy combines all three funnels for flexibility in retirement. That allows you the flexibility throughout your lifetime to ensure your plan is running as efficiently as possible.

Visit my site -> finnprice.com

Business Owner Education on a Weekly Basis -> Newsletter

Subscribe to the Youtube Channel for more video content -> Finn Price Youtube

About the author: Finn Price, CPFA, CEPA, is a business owner and wealth manager at Railroad Investment Group. He helps successful entrepreneurs & individuals with concentrated stock positions in their 30s, 40s and 50s build, organize, protect and transfer their wealth.

Note: this article is general guidance and education, not advice. Consult your money person or your attorney for financial, tax, and legal advice specific to your situation.

Securities and advisory services offered through LPL Financial, a registered investment Advisor, Member FINRA/SIPC.